Carbon Accounting Methodology

Methodology Overview

4tomorrow uses the GHG Protocol Corporate Accounting and Corporate Value Chain (Scope 3) Reporting Standard. These are aligned with the principles of corporate emissions disclosure found in the GRI Sustainability Reporting Standards. We also reference and adhere to internationally recognised and applicable standards such as the Task Force on Climate-Related Financial Disclosures (TCFD), and region-specific standards such as Climate Active & Toitū.

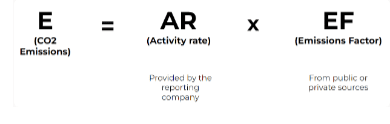

We use various emissions factor databases (such as MRIO, EEIO & LCA), which are constantly updated to assess client-supplied spending and activity-based data. We break down emissions by Scope 1, 2 and 3 and categorise carbon intensity by vendor or activity. From this analysis we can develop an emissions reduction strategy that aligns with the Science Based Targets initiative (SBTi).

Methodology

4tomorrow measures emissions according to standard carbon accounting principles:

- Relevance: Select the appropriate emissions sources, data and inventory boundaries that reflect the emissions impact of the entity and its value chain.

- Completeness: Identify and account for all relevant emissions sources and activities within the inventory boundaries (Scope 1,2 & 3). Where exclusions are required, they are disclosed and justified.

- Consistency: Use consistent methodologies and assumptions over time. Any changes to methods will be documented and declared.

- Transparency: Disclose all relevant methodologies, data sources and assumptions to ensure an auditable trail

- Accuracy: Reducing and quantifying uncertainties as far as possible. Achieving sufficient precision to enable intended decisions

Boundary setting:

Boundary setting is important for accurate carbon accounting. It is defined in the GHG Protocol for Corporate Standards, which defines the scope of activities included and excluded from your organisation’s emissions inventory. There are two main approaches to setting a boundary:

- Financial Control: All operations where the organisation has the full authority to introduce and implement policies and measures are included.

- Organisational Control: The organisation includes emissions from operations based on financial ownership – where it has the ability to direct financial policies to gain economic benefits.

Accurate boundary setting is crucial as it supports completeness and transparency in accounting reporting and prevents misleading findings by shifting emissions off an organisational inventory.

Emissions identification & calculation:

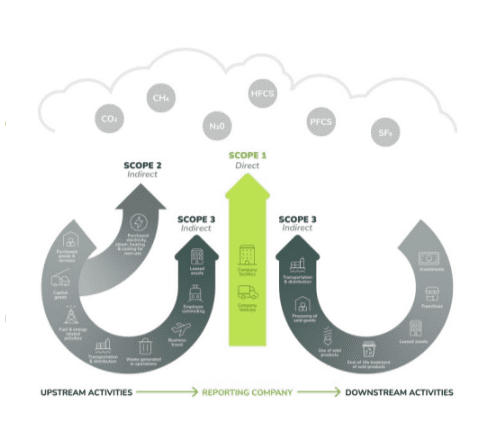

Once organisational and operational boundaries have been established, the next key step is to identify emission sources and accurately calculate the greenhouse gas emissions associated with activities within the inventory. To align with GHG Protocols, companies reporting their carbon footprint must include Scope 1, 2 and relevant Scope 3 emissions.

Scope 1: Direct emissions include any energy source that is burned at an organisation or within a vehicle.

Scope 2: Indirect emissions that occur as a consequence of an organisations energy generation (i.e electricity usage on-premises).

Scope 3: Indirect emissions of upstream and downstream activities occurring throughout the value chain of an organisation. Scope 3 emissions are identified in 15 categories and must include Category 1: Purchased goods & services.

Assessing the relevance of remaining Scope 3 emissions adhere to the following principles outlined in the GHG Protocol Corporate Value Chain Accounting and Reporting Standards.

4tomorrow relies on the data supplied by our clients and includes or excludes elements of this data using the following decision rubric:

- Relevance: The significance of the category to absolute or sector emissions. Consider business goals.

- Magnitude: Assess the size of emissions for each category relative to the total inventory. Set significance thresholds.

- Influence: Consider the potential to influence category emission reductions. Greater influence increases relevance.

- Risks: Categories with financial/strategic/climate risks should be deemed relevant.

- Stakeholders: Relevance noted by stakeholders indicates importance.

4tomorrow currently excludes the following Scope 3 emissions categories from our analysis:

- Category 10. Processing of sold products

- Category 11. Use of sold products

- Category 12. End-of-life treatment of sold products

- Category 15. Investments

Where primary activity data has gaps or inaccuracies that limit calculation accuracy, 4tomorrow will employ robust data quality checks and conservative estimations based on historical data trends and benchmarks to maintain compliance with completeness principles to avoid underestimating emissions

- Activity-based Approach: Calculates emissions based on the raw data that can be specifically quantified into emissions data. This approach is the most accurate as it removes any estimations or assumptions.

- Spend-based Approach: Uses financial expenditure on purchased goods/services to estimate emissions using economic input-output emission factors per dollar spent. These factors can come from various databases. 4tomorrow, we will apply the data set best suited to the activity and region to get the best estimate of carbon emissions

Emissions reduction strategy:

Key elements of 4tomorrow tracking and reporting are:

- Annual emissions inventory and quarterly collection of activity data.

- Maintaining an internal GHG information management system to track performance over time.

- Establishing an emissions baseline year and setting SBTi-aligned targets to progress towards decarbonisation.

- Monitoring performance indicators for defined emissions reduction goals.

- Disclosing all methodologies, exclusions, significant uncertainties, and changes to inventory boundaries, methods or other relevant factors in auditable, public reports.